Global Market Commentary January 2025

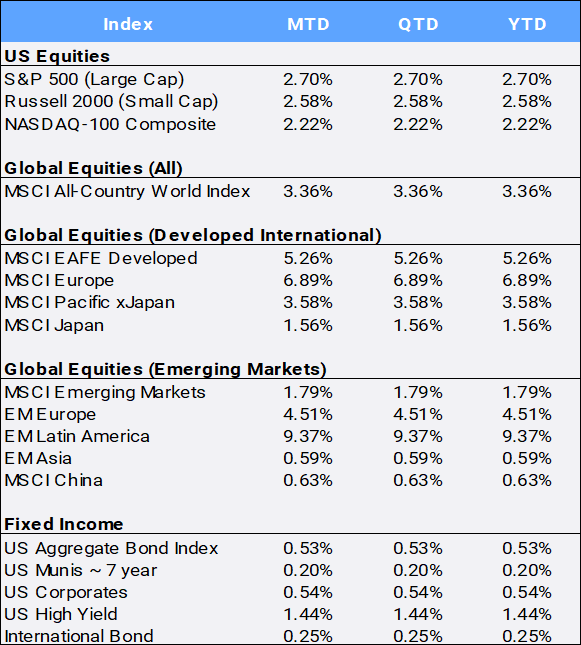

Global stocks came out of the gates strong, gaining 3.36% in January following impressive back-to-back years that saw them gain 22.20% in 2023 and 17.49% in 2024. This represented a nice rebound from last month that saw the MSCI All Country World Index’s (ACWI) decline 2.37% in December. ACWI also made a new trading high on January 24th. In the US, the large cap S&P 500 gained 2.70% in January, but a broadening out was evident as the “average stock” (as represented by the S&P 500 equal weight index) climbed 3.40% this month. Value stocks outperformed growth as rotation was evident with the Russell 3000 Value Index gaining 4.36% versus 2.00% for its growth counterpart. Investor nerves seemed to ease a bit from the start of the year, as evident of the CBOE S&P Volatility Index (VIX), often referred to as “the fear index”, finished the month at 16.43, down 5.30% from where it ended 2024 at 17.35. Still, this was an uptick from the 14.85 low it traded on January 23rd, as angst built by month end on the threat of President Donald Trump leveling 25% tariffs on neighbors Canada and Mexico, alongside a 10% duty on trade with China.

Source: Bloomberg Pricing Data, as of January 31, 2025

Ten of the eleven sectors posted gains in January, led by healthcare (+6.79%), financials (+6.56%) and communications (+5.84%). Technology was the only sector in the red, falling 0.69%. It plunged more than 5% on January 27th sparked by developments out of China’s DeepSeek artificial intelligence startup before clawing back most of the quick selloff by month end. The release of a cheaper cost-efficient AI models from China initiated a hotly contested debate about future chip demand. Mixed earnings from technology mega-cap fueled volatility in the sector. Nvidia and Apple were the two worst contributors to ACWI returns this month falling 10.59% and 5.76%, respectively, whereas the largest positive contributors to ACWI returns were Meta, Amazon, and Alphabet, which climbed 17.71%, 8.34%, and 7.78% respectively in January.

Bonds inched higher this month, as the US Federal Reserve left its interest rate unchanged borrowing rates steady at its first meeting of the year, pointing to continued inflation risks despite pressure from President Donald Trump to cut rates. Fed Chairman Jerome Powell said at his press conference that the central bank will need to see “real progress on inflation or some weakness in the labor market before we consider making adjustments” to its key rate. The Fed’s preferred inflation gauge, the Personal Consumption Expenditures Price Index (PCE) increased 0.3% from the previous month, and 2.6% annualized – which marked an acceleration from the prior month’s 2.4% annual increase. While Powell expressed optimism for progress on lowering inflation but he also noted that being set up for it is one thing, while having it is another.

In international markets, the European Central Bank lowered interest rates by 0.25% to 2.75% and kept the door open for further easing as concerns over lackluster growth supersede worries about persistent inflation. Europe’s economy saw no growth in Q4 2024, while Germany and France—the region’s two largest economies—contracted slightly over the same period. Still, European developed equities carried international markets higher as MSCI Europe outperformed in January gaining 6.89%, pulling MSCI EAFE up 5.26%. Meanwhile, the Bank of Canada reduced its benchmark rate by 25 basis points to 3%, citing US trade policy as a major source of uncertainty. The Canadian dollar is trading around five-year lows versus the US greenback at $1.4477CAD/USD.

Gold surged past $2,800/oz and gained 6.63% in January as tariff threats reignited its record rally fueled by a rush to safety on heightened concerns about global economic growth and inflationary pressures. This follows the safe-haven asset’s 27.22% gain last year, which was its best annual return since 2010. The diversified Bloomberg commodity index increased 3.95% following last year’s 5.38% gain. Meanwhile, oil rose 1.13% this month. Canada and Mexico are the two largest crude oil exporters to the US, but it is unclear if oil would be included among the tariffs. Meanwhile, their equity markets gained 2.80% and 3.60% MTD respectively.

In China, deflation pressures persist, highlighting the need for more possible government stimulus. Its equity market inched along 0.63% this month. Meanwhile, Latin America stood out in EM as the region shot 9.37% higher. Brazil was the largest positive contributor to EM returns gaining 12.42% MTD in a slight rebound following it being the largest detractor to 2024 EM returns, falling 29.77% last year on growing concerns tied to the country’s swelling deficits.

Lastly, Bitcoin surged 8.96% to start 2025 following its impressive 2024 campaign that saw the largest crypto currency gain an eye-popping 123.47% last year. It made a new record above $110k before pulling back slightly as traders took stock of a possible US strategic reserve for cryptocurrency.

Disclosure Statement

Perigon Wealth Management, LLC (‘Perigon’) is an independent investment adviser registered under the Investment Advisers Act of 1940. More information about the firm can be found in its Form ADV Part 2, which is available upon request by calling 415-430-4140 or by emailing compliance@perigonwealth.com

Performance

Past performance is not an indicator of future results. Additionally, because we do not render legal or tax advice, this report should not be regarded as such. The value of your investments and the income derived from them can go down as well as up. This does not constitute an offer to buy or sell and cannot be relied on as a representation that any transaction necessarily could have been or can be affected at the stated price.

The material contained in this document is for information purposes only. Perigon does not warrant the accuracy of the information provided herein for any particular purpose.

Additional Information regarding our investment strategies, and the underlying calculations of our composites is available upon request.

Data Source: Bloomberg Pricing Data, as of January 31, 2025.

Article Source: Perigon Wealth, "Global Market Commentary January 2025" | Written by Jonathan Masse