Global Market Commentary – February 2025

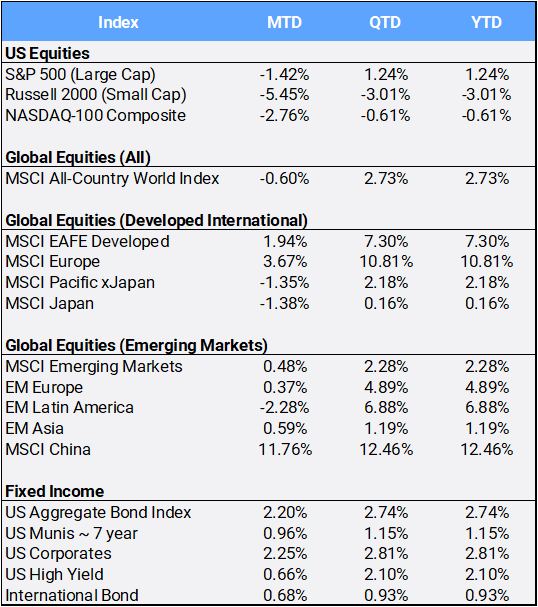

Global equities slipped 0.60% in February, chipping away at their strong January 3.36% start to bring YTD returns to 2.73%. The MSCI All Country World Index’s (ACWI) made five new trading highs this month, but it wasn’t enough to overcome a pullback in US stocks. Heightened uncertainty around government policy, a selloff in growth stocks, and concerns of a consumption slowdown left US indices lower for the month, with the S&P large cap index down 1.42% and Russell small cap stocks off 5.45% MTD. The broad-based tech-heavy Nasdaq Composite index had its worst month since April 2024 as it fell 3.97% in February. Tariffs continued to weigh on markets with the White House stating that the planned levies on Canada and Mexico would take effect March 4th.

Click the image to view the chart larger.

Source: Bloomberg Pricing Data, as of February 28, 2025

Six of the eleven sectors posted gains in February, led by Consumer Staples (+5.09%), Real Estate (+4.22%), and Energy (+3.80%). Consumer Discretionary (-7.01%) and Technology (-2.26%) were the laggards. Style indexes told conflicting stories as the S&P 500 Growth index dropped 2.91% this month to bring YTD returns into the red at down 0.30%. Whereas its S&P 500 Value counterpart actually gained 0.43% in February to bring its YTD gain to 3.33% so far in 2025.

The CBOE Volatility Index, often referred to as the market “fear gauge”, jumped 19.48% to close February at 19.63 – after trading as high as 22.40 at one point on the last trading day in February. Geopolitical risks elevated following a clash in the Oval Office as President Donald Trump Vice President JD Vance argued with Ukraine President Volodymyr Zelenskyy during an extraordinary moment in front of the global media regarding a possible rare earth mineral rights deal – which investors hoped would be a precursor to possible peace in its war with Russia.

Most international markets closed earlier on February 28th just before the infamous shouting match between the leaders mentioned above. Still, both developed and emerging markets diverged away from the US selloff, as those regions gained 1.94% and 0.48% respectively in February. The pan-European Stoxx 600 bell weather index secured a ten-week winning streak. Helping the regional market outlook is the prospect of a new German government that may cut taxes and lift spending, solid earnings reports, and optimism of a resolution to the war in Ukraine (again, most of Europe markets were closed before the Oval Office disagreement). In emerging markets, China led equity markets gaining 11.76% in February even before their 10% US tariffs are scheduled to also hit in early March. Unlike their US counterparts, Chinese technology stocks have been surging with a turning point after Chinese President Xi Jinping met with entrepreneurs this month. The rare-sit down included Alibaba founder Jack Ma, as was viewed as a signal of assurance and stability after a crackdown on the technology industry in recent years.

The US Aggregate Bond index jumped 2.20% in February, as traders searched for safety in a month that hit its crescendo following the Trump-Zelenskyy spat. Bond yields were down almost 5% across the curve this month as the 2-year rate closed February at 3.99%, the 10-year at 4.21% and 30-year at 4.49%. Those key rates started 2025 at 4.24%, 4.57%, and 4.78% respectively. Yields and prices move in opposite directions.

Gold, a non-yielding asset, can often “shine” as interest rates decline. The precious metal is also often viewed as another “safe haven” asset in troubling times. It hit an all-time high of $2,956.22/oz as it gained 2.20% in February to bring YTD returns to 8.89%, boosted broadly by concerns over the Administration’s tariff plans. The diversified Bloomberg Commodity index was up 0.78% MTD and is up 4.76% on the year, despite oil – a main component of the index – falling 3.82% this month to bring YTD returns to down 2.73%.

Last, Bitcoin, which is often referred to as “digital gold” plunged 17.53% in February in its worst month since the FTX collapse in 2022. The largest crypto currency is also reeling from the recent theft of $1.5B by North Korean hackers from the Bybit exchange. YTD returns were brought in the red to negative 10.14% and is off more than 25% since its all-time high reached in January on President Donald Trump’s inauguration day.

Disclosure Statement

Perigon Wealth Management, LLC (‘Perigon’) is an independent investment adviser registered under the Investment Advisers Act of 1940. More information about the firm can be found in its Form ADV Part 2, which is available upon request by calling 415-430-4140 or by emailing compliance@perigonwealth.com

Performance

Past performance is not an indicator of future results. Additionally, because we do not render legal or tax advice, this report should not be regarded as such. The value of your investments and the income derived from them can go down as well as up. This does not constitute an offer to buy or sell and cannot be relied on as a representation that any transaction necessarily could have been or can be affected at the stated price.

The material contained in this document is for information purposes only. Perigon does not warrant the accuracy of the information provided herein for any particular purpose.

Additional Information regarding our investment strategies, and the underlying calculations of our composites is available upon request.

Data Source: Bloomberg Pricing Data, as of February 28, 2025.

Annual Form ADV

Every client may request a copy of our most current Form ADV Part II. This document serves as our “brochure” to our clients and contains information and disclosures as required by law.

Perigon Wealth Management, LLC is a registered investment advisor. Information in this message is for the intended recipient[s] only. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy will be profitable. Please click here for important disclosures or visit our website at perigonwealth.com.”

Article Source: Perigon Wealth, "Global Market Commentary February 2025" | Written by Jonathan Masse